This morning I am just taking a walk through the markets, kicking tires and turning over rocks, in the constant search for opportunities.

Rather than bore you with more data from the Fed or discussions of conditions in the banking industry right now, I thought I would just share a few ideas I have been tracking that are probably worth accumulating no matter what the markets do over the rest of the year.

A Hedge Against Inflation

Alico (ALCO) owns something that is in very high demand right now. They have about 100,000 acres of land, mostly right here near me in Southwest Florida.

Almost half of the properties are used for citrus crops, the biggest being oranges. Most of the crop is sold to Tropicana for the “not from concentrate” fresh juice market.

They also own over 50,000 acres of land that they lease for cattle grazing, recreational hunting, farming, and mining. They have also been steadily selling parcels to the state government for conservation purposes. So far Florida has bought 22,000 acres of land from Alico.

All told, Alico has sold more than $86 million worth of land over the last 3 years.

They have been using that cash, along with cash generated from the citrus business, to increase their dividends, buyback stock, and reduce debt.

They have also been buying more orange groves as they recently bought 3,300 additional contiguous orange grove acres. The company just resigned a long-term deal with Tropicana so the orange juice business should continue to produce cash for years.

Let’s be clear, this is not a flashy, get rich overnight stock…

Alico is going to continue selling land for conservation, and I suspect that at some point the prices will be too attractive not to start selling for development.

Buy every time there is market disruption for some reason or another. Reinvest the dividends and just let time do its thing.

If inflation does break out of its cage next year, land prices could escalate quickly, driving up share prices much faster than the street is anticipating.

I will also point out that after a long period of being relatively quiet, Alico has been doing a lot of roadshows over the past year to drum up investor interest.

A Company With Red Flags but Much Potential

Golar LNG (GLNG) is a 75-year old company that owns and operates Liquefied Natural Gas (LNG) carriers.

The company’s shares continue to trade at a massive discount to any reasonable estimate of the assets that they own.

B. Riley analysts put the value at $20.50 a share while the estimate out of Stifel is $24.

As of today, the stock is trading right around $11 per share.

The stock has upset a lot of investors over the last five years, but it is obvious this company is not being properly valued by the market.

Golar is in a great position to focus on its Floating Liquid Natural Gas (FLNG) business. The board is also talking about possibly separating the upstream FLNG business from the midstream shipping business if the outlook and pricing in shipping continue to improve.

The sudden resignation of the CEO recently is troubling but the analysts seem to agree that it is not a negative development.

Golar is not without risks but the assets are on sale and it is only going to take a hint of good news for the shares to jump higher.

A Bet on the Future of Food

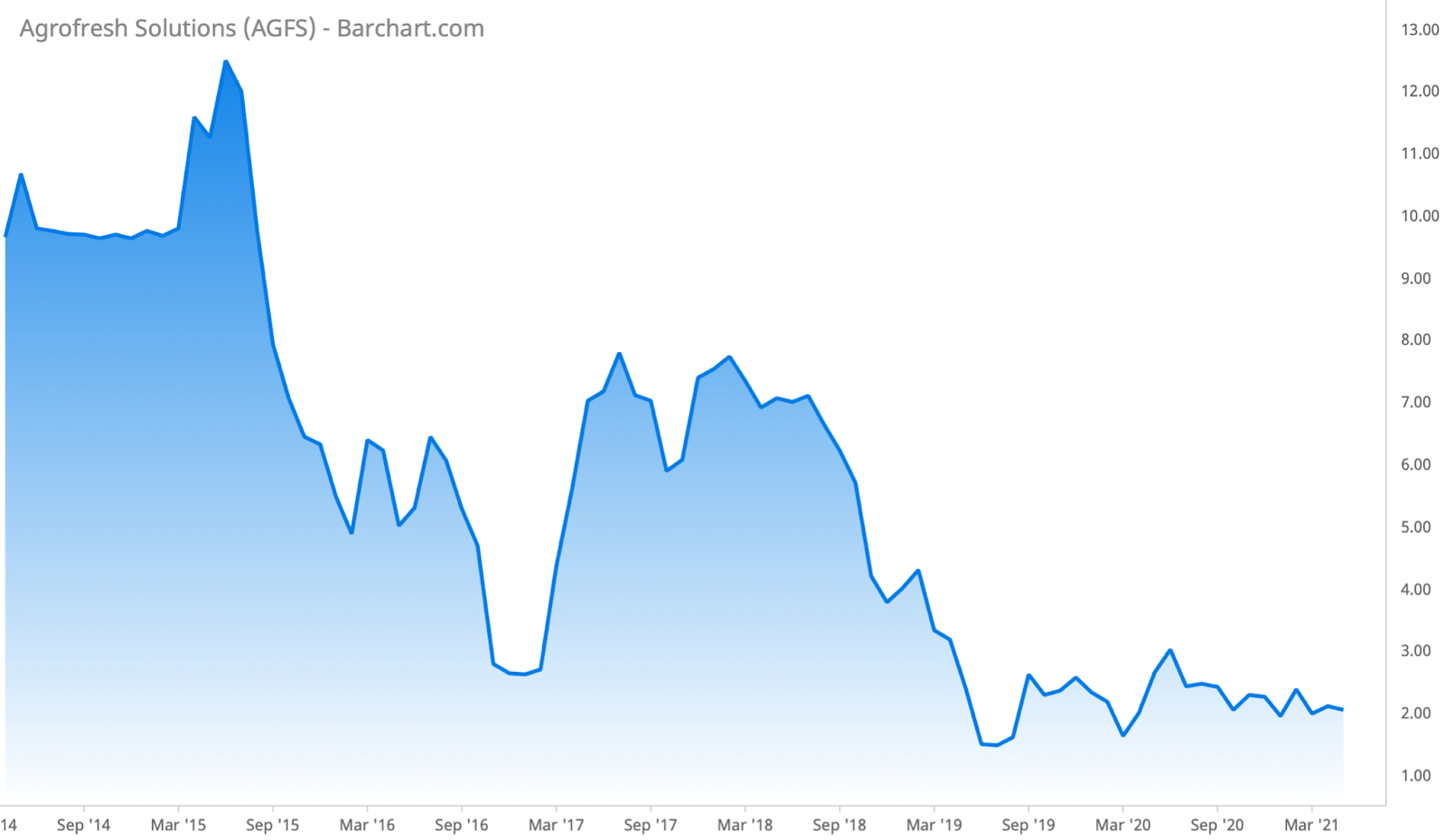

Finally, while doing my weekly research I noticed that there has recently been a CEO change at AgroFresh Solutions (AGFS).

AgroFresh is an interesting business as they provide science-based technologies that extend the shelf life of fresh produce. AgroFresh used to be a wholly owned subsidiary of Dow Chemical which still owns more than 40% of the company.

AgroFresh does business in more than 50 countries around the world.

Their patent portfolio of over 500 granted and applied for patents is not even vaguely factored into the current stock price in my opinion.

Reducing food waste is a big deal in today’s world and Agrofresh products can help achieve that goal. This could (and should) turn into a high growth stock over the next few years.

The rumor is that the CEO change is Dow putting someone in the seat that can make that happen.

Now, I don’t suggest betting the farm on AgroFresh Solutions, but this is a $2 stock whose products have a total market opportunity measured in the billions of dollars.

There is also a better than average chance that some other company in the Agricultural and Chemical business just buys the whole company to enhance their portfolio at some point.

Best,

Tim