On June 2, 2012, the three-masted, steel-hulled ARA Fragata Libertad set sail from Buenos Aires, Argentina to make its annual training voyage.

Recent graduates from the Escuela Naval de Argentina were on board, along with 69 members of the Argentine Navy, and a crew of 220.

The 338-foot navy vessel – one of the largest and fastest sailing ships in the world – docked at ports in Brazil, Suriname, Guyana, Venezuela, Portugal, Spain, Morocco, and Senegal before the unthinkable happened.

Tuesday, October 2, 2012, was supposed to be just another routine day of training for those on board.

That was until they attempted to leave the Port of Tema in Ghana.

Weapons were drawn…

And one of the oddest events of the 21st century ensued.

After learning from Ghana officials that their ship had been “seized,” the cadets on board quickly found themselves in the middle of an epic battle.

Now, this wasn’t a fight between countries raging to go to war… no, think again.

Instead, the sailors found themselves in the middle of a battle between their very own government and – believe it or not – a U.S.-based Hedge Fund run by a ruthless chap named Paul Singer.

Elliott Management vs. Argentina

For Paul Singer and his team over at Elliott Management, foreclosing on a 1950’s warship – as crazy as it sounds – was just another day at the office.

The story of this foreclosure is actually pretty straightforward.

In 2001, the Argentinian government issued some debt.

And Singer, who has no problem pillaging money using methods that others might find displeasing, saw this debt offering as an opportunity.

Singer was well aware of the tremendous financial pressure a country like Argentina was facing. He learned from experience that many countries, particularly poorer ones with corrupt governments and fragile economies, often borrowed far more than they could realistically repay.

In the late 1980s, for example, roughly 50 countries defaulted or had to restructure their debt. This included most of Latin America, and countries like Mexico, The Philippines, Vietnam, and South Africa.

So Singer and his team mapped out a vicious plan to purchase the debt at a very low price and then try to negotiate or sue the country for full repayment on the original terms.

An investor who pursued this strategy came to be known as a “rogue creditor”– a form of activist investing. The strategy could prove extremely lucrative, but only if you had the stomach for it.

Around this time, Argentina was experiencing severe economic depression. Seven out of ten children were living in poverty and unemployment was historically high. In December of 2001, things got so bad that the bank accounts of the citizens of Argentina were frozen, causing violent protests throughout the country. Within a matter of months, five different Presidents cycled in and out of office. One even had to be airlifted out of the country for his own safety.

With that economic backdrop, and only 12 months after Singer placed his bet, sure enough, Argentina defaulted on their debt. Soon after, the country agreed to a restructuring with 92% of the debt holders.

But, as you may have guessed, Elliott Management was not part of that 92%.

Singer wanted his money… and wanted it all.

As long as Elliott Management remained patient, other bondholders would eventually fold, accepting lower terms to make a deal happen. The holdout pool would then shrink and Elliott’s chances of Argentina paying them back would improve over time.

Nearly ten long years later, Elliott was still holding their cards at the table.

Then in 2012, Elliott and a few other debt holders won a series of court rulings in the U.S. and U.K., stating that Argentina must pay up, in full.

Under the court rulings, the remaining bondholders were granted the authority to seize Argentine assets to make up for the debt, similar to how a bank may foreclose on a home if the homeowner doesn’t make payments.

So, just like that, the merciless Paul Singer started a series of attempts to seize Argentinean government assets.

The modern-day pirates of Elliott Management weaved across the globe in an attempt to find local courts that would grant orders for it to take possession of Argentina’s property as collateral for the unpaid debts.

They attempted to seize Argentina’s central bank reserves…

Pension fund assets…

Even a satellite launch slot in California that was under contract with SpaceX, the private space firm owned and operated by Elon Musk.

Each step along the way, Argentinian lawyers raced to the local courts to block the seizure.

This string of events leads us right back to that Tuesday morning on October 2, 2012, in Ghana’s Port of Tema.

Elliott Management had been tracking the ship, awaiting its arrival in a port that would honor the rulings of the U.S. and U.K. courts. And in the knick of time, just before Argentina could deploy their best lawyer, Ghana complied and supported the demands of Elliott Management.

As the story goes, Singer and his team successfully orchestrated the seizure of one of Argentina’s most prized possessions, the ARA Fragata Libertad.

The training navy vessel remained dockside at the Port of Tema for over a month. Most of the cadets left the ship, but the Argentine soldiers remained on board while the two sides locked horns in court.

Eventually, the International Tribunal of the Law of the Sea invalidated Elliott’s court order, and the ship sailed away.

The cat and mouse game between Argentina and Elliott Management continued for years until a much more business-friendly President, Mauricio Macri, was elected and made negotiating with the holdout hedge funds a priority.

Elliott Management had spent a total of fourteen years on the legal fight, but in the end, it was well worth it.

Argentina agreed to pay the company $2.4 billion, a 1,270% return on its initial investment, according to one analyst.

The result sent a strong message:

Singer always wins.

To this day, whenever Paul Singer’s Elliott Management buys into a company, the firm has only one objective – to make the share price go up.

And to do that, it’ll do whatever it has to do, combative or otherwise, even if that means foreclosing on a naval warship.

Who are Paul Singer and Elliot Management?

Paul Singer and his team at Elliott Management have been in the activist game for a very long time.

The firm was started back in 1977 as a convertible bond arbitrage shop. In the aftermath of the explosion in the junk market caused by the collapse of Michael Milken and Drexel Burnham, Elliott Management turned towards distressed debt investing and corporate restructuring. Singer and his team have been involved in several of the better-known restructuring of all time, including TWA, MCI, WorldCom, and Enron.

Distressed debt back in the early 1990s was no place for sissies. Today, investing in distressed issues can be a very polite game involving well-dressed lawyers and bankers. But back then, there were a lot of sharp elbows.

Hillary Rosenberg’s excellent book The Vulture Investors does a great job of telling the story of the distressed debt investors of that time. It was a rough and tumble market, and those that emerged as winners made a lot of money for themselves and their investors.

Paul Singer’s Elliott Management was one of the winners.

As the amount of distressed debt began to decline over the last couple of decades, Singer turned his company into a multi-approach fund that used several strategies. One of those strategies has been activist investing.

Singer is an aggressive activist and has not hesitated to pick fights with big companies like Twitter (TWTR), Hess Oil (HESS), Telecom Italia, Samsung, and even Warren Buffett over the years. He has won far more of these battles than he has lost, and his investors have benefited.

Elliott has little reason to back down from mere corporations. As we discussed earlier, his firm has tackled entire nations before and won the fight.

His battle with Argentina wasn’t the only successful sparring round…

- Elliott once bought $20 million face value of defaulted Peruvian bank debt. They then took Peru to court and eventually won a settlement of $58 million.

- While trying to collect $100 million in defaulted bank debt from the Republic of Congo, Elliott exposed widespread corruption in the street. The courts eventually awarded Elliott over $90 million for debt that they paid $32 million for.

I don’t see an activist investor who once stole a warship from a sovereign nation losing much sleep over a pissed-off CEO or a hostile board of directors.

Singer’s experience of activist investing is clearly in a league of its own.

Singer’s Next Target

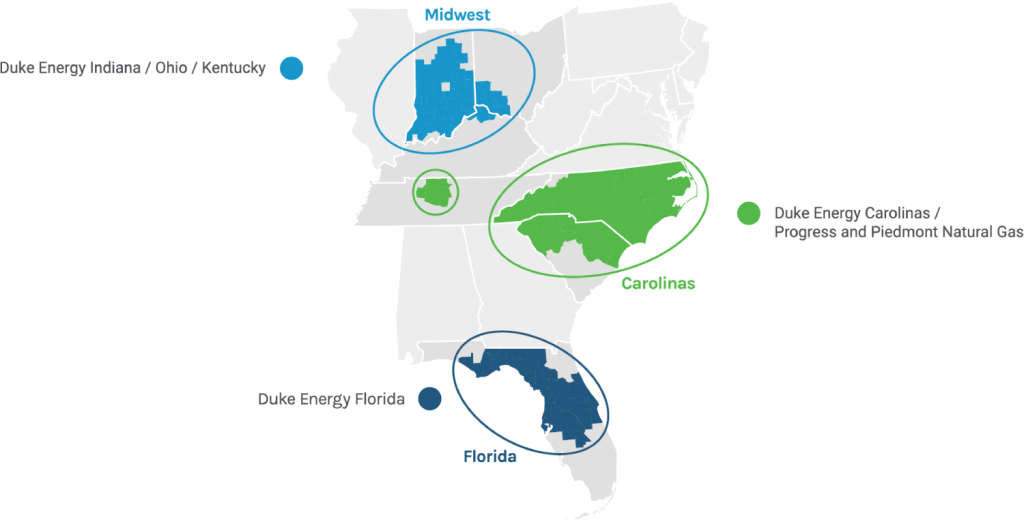

Elliott has gone big this time. Their newest target is Duke Energy (DUK), one of the largest utility companies in the United States.

Duke has operations in the Carolinas, Florida, and the Midwest. The company services more than 1.6 million customers.

Like most utilities, they use a range of fuel sources, including coal, hydroelectric, natural gas, oil, and nuclear fuel, to produce electricity for their customers.

Duke also owns a portfolio of renewable energy facilities including solar, wind, and fuel cell operations.

Elliott’s campaign targeting Duke all started last month when the fund sent a letter to the board of directors suggesting they make changes. Singer’s team believes they could unlock as much as $15 billion in shareholder value. They claim to be one of Duke’s ten largest shareholders, which means that they have a stake of about $1 billion in the utility company.

The letter notes that Duke owns a collection of the highest-quality and most under-appreciated collections of utility franchises in the country. In addition, their franchises are located in areas considered to be some of the high-growth regions of the country.

According to Elliott management, given the attractive franchises they own, Duke should be performing a lot better than they are.

In their letter, they state:

“Our extensive diligence and conversations with stakeholders have made it clear that the Company’s sprawling, noncontiguous portfolio of utilities has burdened shareholders with a “conglomerate discount” relative to the value of Duke’s utility franchises. Duke’s current ownership of utility businesses across three separate geographies has delivered few benefits for stakeholders and has left its Florida and Midwest utilities undermanaged and undervalued.”

The letter also points out some of the more egregious missteps and accidents on management’s watch that have cost the company billions of dollars. These include the Atlantic Coast Pipeline cancellation that caused a $2.1 billion write-off and an overpriced acquisition of Piedmont Natural Gas back in 2016.

The solution, according to Elliott, is for Duke to split its current operations into three separate companies.

The Florida assets should be in one company…

The Carolinas would be another…

And the Midwest would be the third.

Elliott thinks that separate management teams would do a better job of operating a smaller regional utility than the current management is doing with the current widespread operations.

According to the letter:

“Duke should appoint new highly qualified independent directors to lead an unbiased review of the value potential from a tax-free separation into three regionally oriented utility holding companies — the Carolinas, Florida, and the Midwest. In our view, each of these pro forma entities would have meaningful scale, and we are highly confident that this structure would create substantial value for shareholders and position Duke to best serve its stakeholders.”

Elliott thinks that there would be immediate valuation upgrades after the split, adding at least 20% to the current value of the shares. That would be followed by even more long-term appreciation as more focused, locally aware management drove improvements in the business.

Elliott has asked for seats on the board to help put the following plan into action:

I think Elliott is right in their assessment of Duke’s conditions and prospects. As Elliott adequately mapped out, the company would clearly function better as three divisions than it is currently doing as one.

In its response letter, Duke pointed out that its aggressive move into clean energy is driving above-average returns over the past two years.

They also pointed out:

“Duke Energy’s strategic goals are supported by its history of strong safety and operational performance, and excellent customer services, allowing it to consistently pay shareholders a dividend, which the company has increased for 15 consecutive years.”

In reality, Duke’s stance on “excellent customer services” doesn’t necessarily hold true.

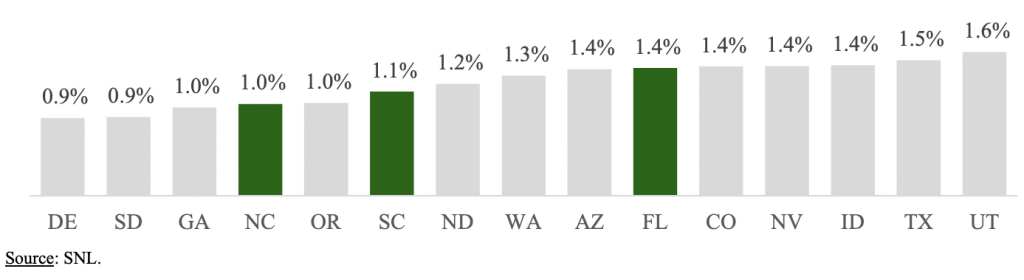

As pointed out in Elliott’s letter, Duke Energy Florida’s customer satisfaction scores actually consistently rank in the bottom two among large utilities in the Southeast.

This is just another example of leverage, that of course, sides with the already strong argument outlined by Singer’s team.

The board of Duke can yawn at Elliott’s position on the matter all they want, but to me, standalone utilities implementing more focused, high-performance strategies to benefit their respective home jurisdictions makes a lot of sense.

A focused, truly local utility company would be better positioned to serve the needs of customers and build more constructive regulatory relationships.

And to be frank, I have a hard time believing that the majority of Duke shareholders – amongst other things – will disagree.

A Win-Win Opportunity

I look at this as a special situation as a win-win trade.

If Elliott prevails, you will see a short-term pop in share prices and have the chance to pick and choose which of the three spin-offs you want to own for the long run. You can either hold them all, or just play favorites and keep the one with the highest growth prospects and best renewables portfolio.

Now let’s look at the other side of the equation.

If Elliott doesn’t prevail, you’ll still own a utility company with a recent history of dividend increases and a large presence in three of the fastest-growing markets in terms of population growth in the country.

Duke is a profitable company that doesn’t have to rely on pie-in-the-sky growth scenarios to prop up share prices. Net cash provided by operating activities continues to grow year over year.

Due to the prospect of looming interest rate hikes and inflation, in the near term, profitable companies look more attractive… especially those with “pricing power,” or the ability to pass a price increase to the customer.

If costs for utility companies rise due to inflation, these companies are typically granted rate increases to cover the higher costs and still provide an attractive return for investors.

Because the effects of inflation are passed along to customers, investors in utility stocks are protected from shrinking profit margins.

An added plus is the ability to pay and grow dividends—giving stock owners an ever increasing cash flow.

Duke Energy successfully checks both of those boxes.

And finally, we are reminded that Duke still has many components of a premium utility company.

As Elliott’s activist campaign plays out, Duke can hang their hats on organic growth within its services and territories, their commitment to explore renewables and zero-emitting power generation technologies such as hydrogen and advanced nuclear, and a long pipeline of investment opportunities in critical infrastructure.

Update November 15, 2021: Duke Energy Corp. agreed to add two directors backed by Elliot Management Corp to the companies Board.

Update May 16, 2021: Elliot Management and Duke Energy reached an agreement with Elliot exiting its more than 1 million share stake for ~10% return not including dividends.