Inflation doesn’t matter.

Just ask your friendly Federal Reserve board.

They are very comfortable with inflation levels and their ability to control them. They are even content to let inflation climb over the 2% target rate for some time.

Fed Chair Jerome Powell told Congress last month that:

We have been living in a world of strong disinflationary pressures, around the world really, for a quarter of a century. We don’t think a one-time surge in spending leading to temporary price increases would disrupt that.

What he’s saying is that because we’ve kept inflation rates low for so long, we can afford to let it run hot – as long as the average rate stays around 2%.

Right on. But this is like saying: “Well, the stock market has only trended up for a quarter century, so we don’t think a surge in unreasonable valuations could disrupt that.”

I don’t think the Fed recognizes that today’s situation is not the same as it was in the aftermath of the Great Financial Crisis.

The amount of stimulus money that has already been thrown into the economy today is multiple times larger than the bailout packages of 2009.

We’ve never printed this much money in such a short period of time.

On top of that, President Biden now wants to add a $2 trillion infrastructure package to the mix.

Once that’s done, he’ll move onto his $1.8 trillion American Families Plan.

That’s a lot of free money being thrown out into the world.

Then consider the Fed and its actions over the past year…

When I look at the M1 money supply, I see that it has tripled since this time last year.

The Fed is adding more via bond repurchases every week.

Again, that a lot of money is being thrown out into the world.

As I seem to recall from basic economics texts, more cash chasing the same level of goods is inflationary.

It’s as simple as that.

The Market’s Biggest Threat

I am reminded of the scene in Game of Thrones when Daenerys Targaryen realizes that her dragon is flying around eating the local livestock and children when she thought she had it under control.

To get an idea of the risky bet that the Fed is making, just imagine if that dragon was named Inflation.

While we’re in uncharted waters, the markets’ biggest threat from inflation right now is the genuine chance it drives interest rates higher.

The Fed can undoubtedly keep its foot on the neck of short-term interest rates by keeping them close to zero.

But it’s the market that will decide the direction of long-term rates.

Much of the bullish argument for the markets is based on the idea of low-interest rates. If rates were perceived as rising steadily, the markets could get very ugly, very quickly.

No one under the age of 70 on Wall Street has managed money during a period of high inflation and rising interest rates. We haven’t seen those two conditions paired together for an extended time since the 1970s.

The combination of higher-rates and inflation could easily spin things out of control.

Perhaps it’s already happening…

Ten-year inflation expectations rose above 2.4% this week, the highest since April 2013.

Treasury yields also rose across the curve, with the benchmark 10-year rate climbing to 1.63%, reversing a trend of consolidation seen in recent weeks.

Right Before Our Eyes

I went shopping the other day and picked up some of the diced ham I use for my daily chef’s salad lunch. I noticed the price of diced piggies was up over 30% in less than a month.

I then refilled my Skippy peanut butter supply, a can of jelly, and bought a box of cereal for my granddaughter.

Those too, were a bit more expensive than usual.

But it appears that’s just the tip of the iceberg.

Next time you’re at the grocery store, you too can check to see if items are more expensive than you last recall. I guarantee you’ll see a difference.

Or, check to see if you’re getting shafted on a costs per unit basis of the items you want to bring home.

For example, a roll of paper towels being sold at Costco may sell for the same price as it was last month, but now, the end consumer is getting less paper towels for their buck.

Inflation first happens without raising prices

— Galactic Trader 💰⚒💰 (@Galactic_Trader) April 26, 2021

Costco paper towels. Same price as the previous several times buying them. Now with 20 fewer sheets.

140/160= .875

Inflation rate: 8.75%https://t.co/4T6Cn4MiO6 pic.twitter.com/5Vf5EDRHTS

You see, inflation is a weird thing.

As prices rise, we’re starting to witness cracks in the economy’s foundation.

Look at housing prices around the United States. All the money the Fed printed is chasing real estate, and housing prices are the hottest they have been in a long time.

Even mythological assets have gotten into the party with DogeCoin, a cryptocurrency that started as a joke, rising from basically zero to as high as $.44 this year.

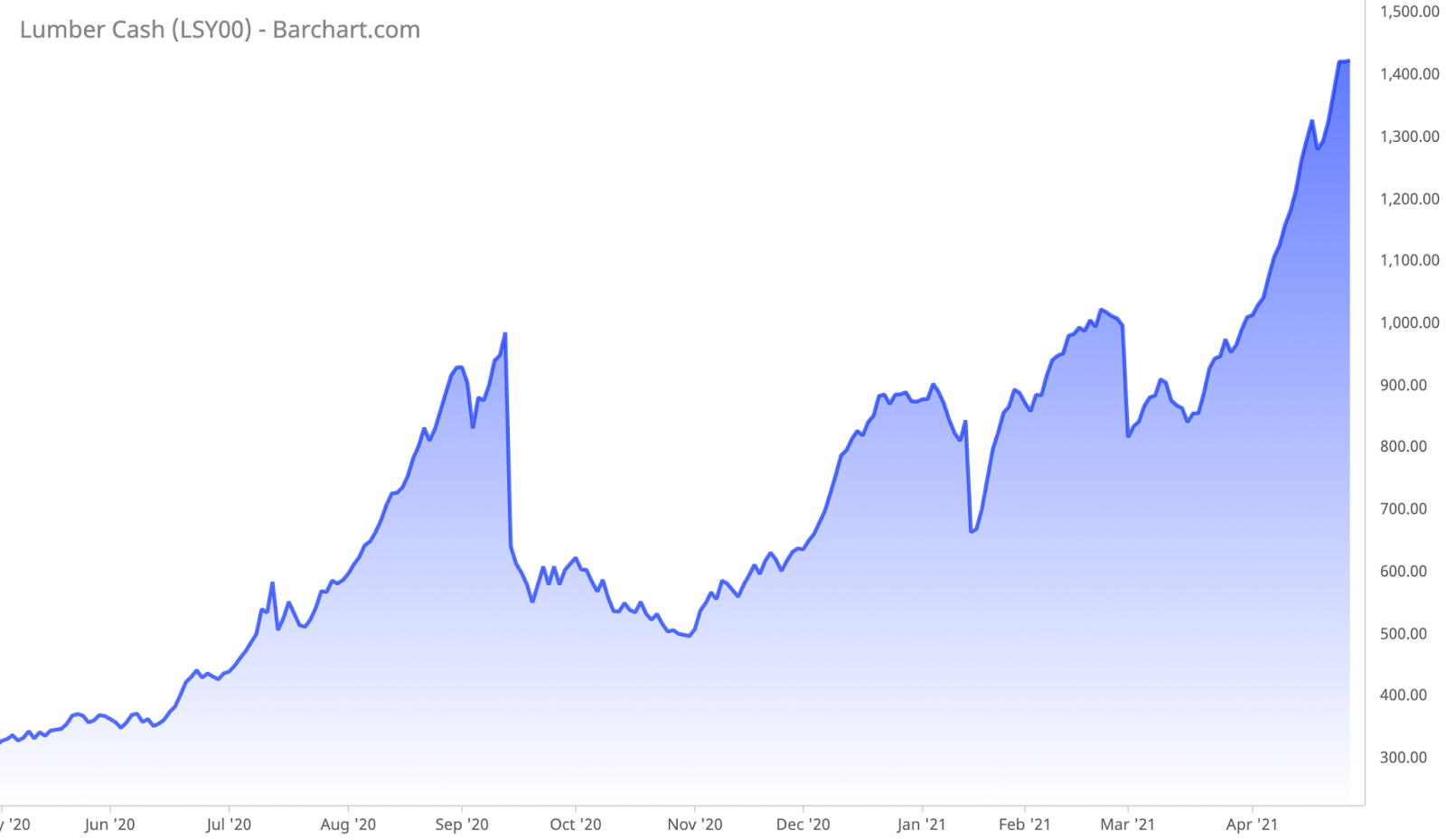

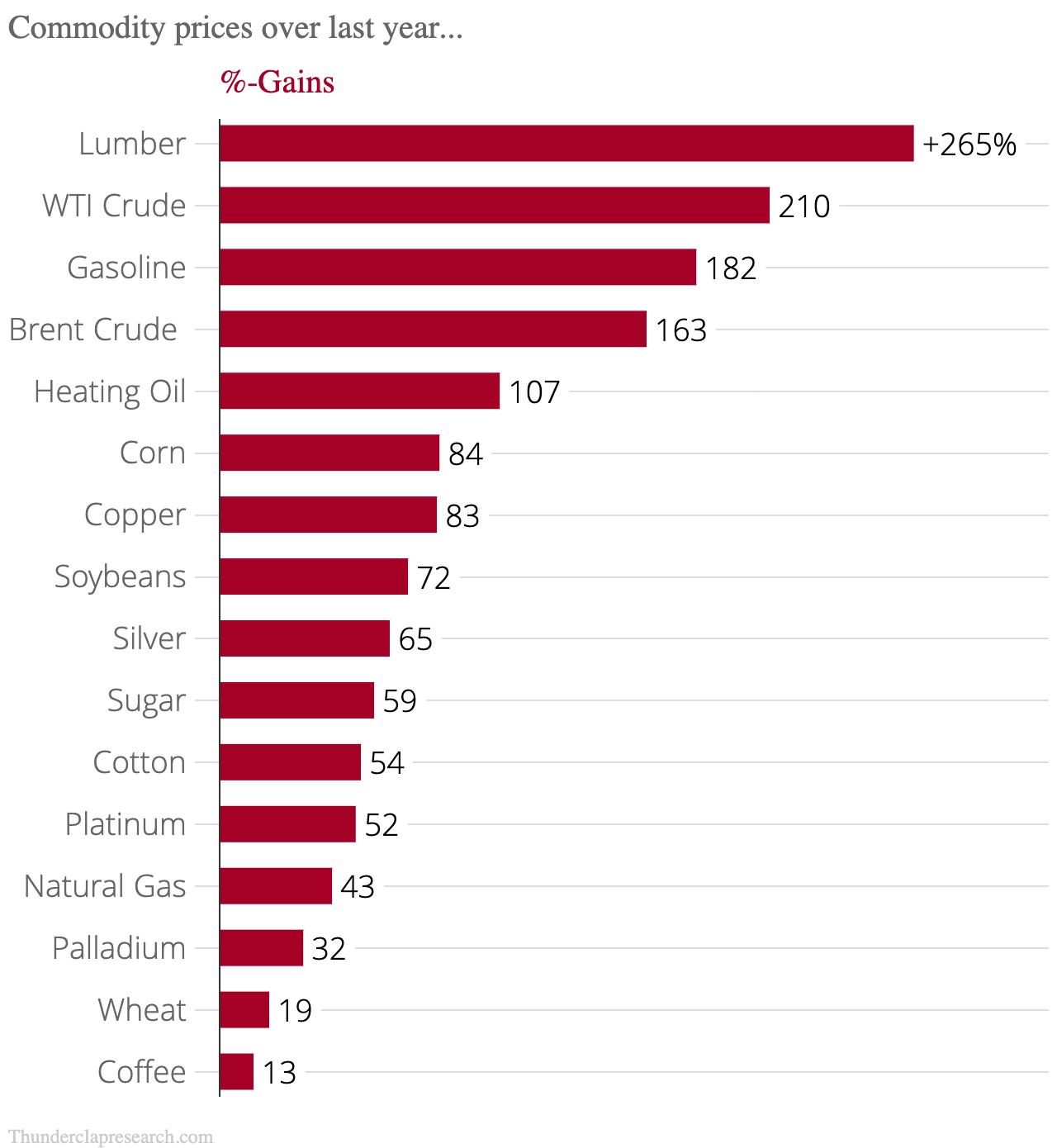

Then, of course, you have to look at what commodities prices have already done in the past year.

Commodities like lumber and copper are climbing at an alarming rate.

Corn prices have risen by 16% so far this month, the largest monthly gain since May 2019, and have risen every month since July, unleashing a 43.7% gain so far this year.

The price of corn is especially important because it is a major input for everything from gasoline to meat to industrial products like wallboard and insulation used in houses.

Keep in mind: The official story from the government – and even some mainstream news outlets – is that the costs of basic goods aren’t rising.

Have they not looked at these numbers?

My point is, inflation may be here already.

It may not be evident on the Feds Consumer Price Index (CPI) prints just yet, but that doesn’t mean it’s not already becoming evident in our very own pocketbooks.

As for the stock market, the questions will be:

Can the Fed control a strong surge of inflationary pressures caused by all the money printing at every level of government?

Will interest rates rise and spook the stock market as a result of price inflation?

The probability of all of these things happening is rising every day. That doesn’t mean they have to happen, just that the odds of it happening are getting higher all the time.

If 2020 taught us anything, it’s that markets will do whatever the hell they want when they want.

How to Protect Your Neck

We can protect ourselves from inflation and rising rates by taking a couple of steps.

First, do not buy stock in any company you are not willing to double and even triple down on in a bad market.

Second, keep a lot of cash. I know returns on cash are nonexistent right now, but cash today is a tool, not an asset.

Third, add some assets that do well when there is inflation and rising rates.

I have talked on several occasions about the Apollo Senior Floating Rate Fund (AFT). All of the loans are floating rates, so the payout will rise if inflation pushes rates higher. The fund trades at a discount to Net Asset Value (NAV) of almost 8% and yields over 6%.

Historically emerging market debt also does very well when inflation pressures the value of the dollar. Templeton Emerging Mkts Income (TEI) is trading at a discount as well with a yield of over 11%.

I also like the Aberdeen Asia-Pacific Income Fund (FAX). The fund owns Asian debt securities and has a discount to NAV of more than 8% and a yield of 7.6% right now.

All three funds pay monthly income and can help protect your portfolio from rising inflation and interest rates.