Let’s talk about business development companies today. For the record I love BDC’s. They are banks on steroids with a lot less regulation.

A business development company (BDC) is a public company that invests in entities that are too small for traditional bond offerings. In short, they help small and/or distressed companies grow in the initial stages of development.

Similar to REITs, BDCs are required to pay 90% of their taxable income in the form of dividends to shareholders.

BDC’s allow individual investors to invest in small to midsize private companies much like private equity and venture capital funds are able to do. Often the loans they make will have some form of equity participation so we can collect fat interest checks and have some exposure to potential upside of the business.

BDC’s really came into their own in the aftermath of the Great Financial Crisis of 2008-2009. Banks decided (in reality were forced) to step away from riskier types of corporate lending, especially in the smaller company segment of the market. Banks could no longer participate, so early-stage growth lending businesses and BDC’s stepped up to fill the void.

A Good Year For BDCs

As the economy continues to open, 2021 could end up being a strong year for well managed BDC’s. Margins should move higher as the Fed keeps a lid on short rates and long rates drift higher.

Already in 2021, we have seen BDCs raise about $2.7 billion at very low rates.

As an example, Golub Capital (GBDC) just issued 6-year bonds at 2.50% and obtained a new senior credit facility at one month Libor +1.5% to start. At the moment that is about 1.61%.

Now GBDC can lend that cash out at 8% and lever it by an additional 50%. You can begin to see just how important locking in low rates can be for BDC’s. You can also start to see how profitable this can be for their investors.

The best BDCs to hold for the long term

BDCs have a history of working with private equity firms to source deals.

And once you factor in the equity participation that is added into many of the loans, a lot of the transactions actually start to look like regular private equity deals.

With that being the case why don’t we just go straight to the BDC’s sponsored by or affiliated with private equity firms? In this article we will take a look at two such cases.

The Upcoming Second Largest BDC in the US

Right now, there is a merger happening that has been over two years in the making.

Now bear with me because this can be a bit confusing…

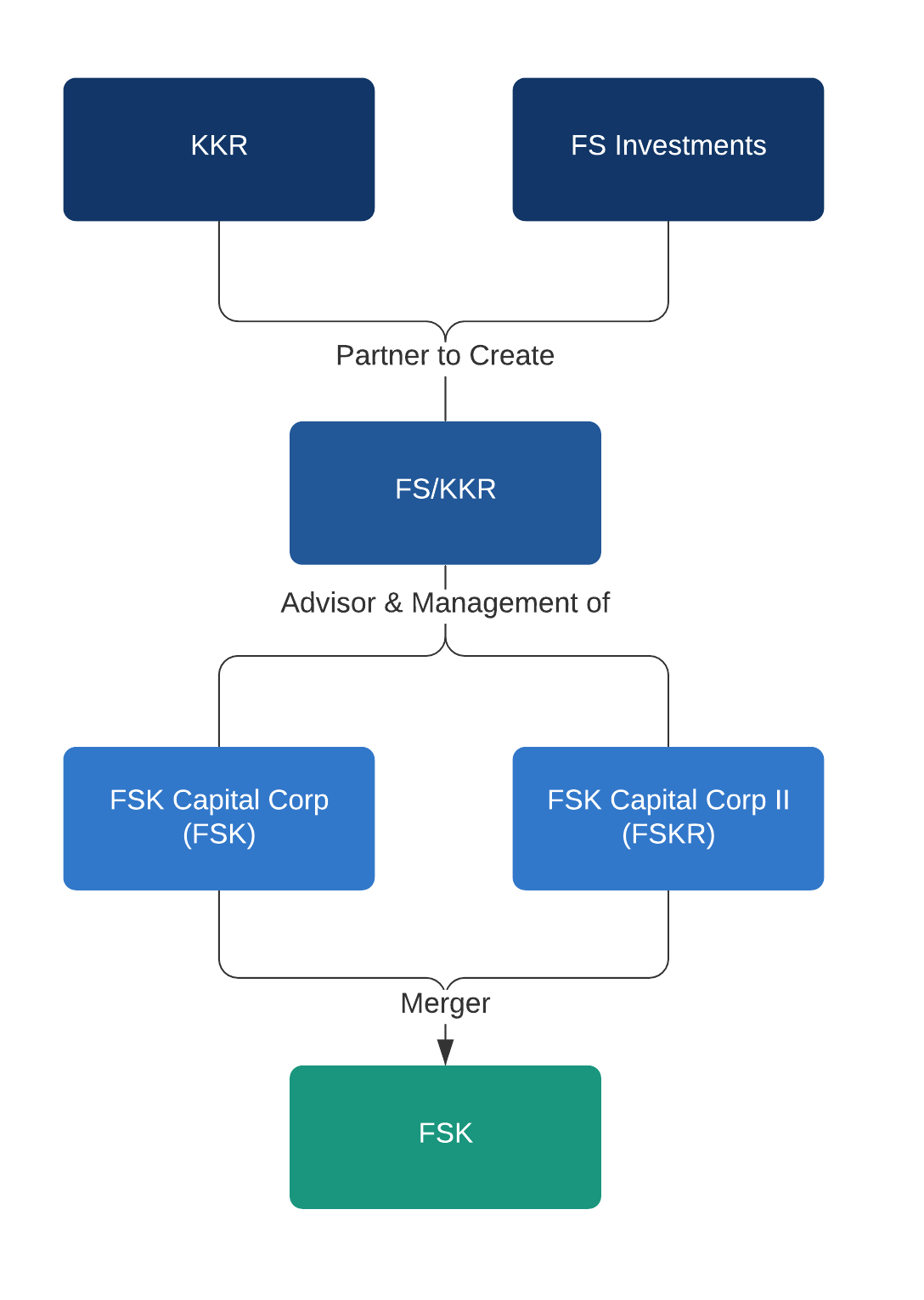

FS Investments is a firm that specializes in bringing alternative strategies usually only available to large institutions to the public. KKR Credit is a division of one of the largest and top performing private equity firms of all time. KKR has borrowed and lent billions of dollars for its portfolio companies so I think they know a little something about middle market lending.

FS Investments and KKR Credit are merging two BDCs that they own and manage together. These entities are FSK Capital Corp. (FSK) and FSK Capital Corp. II (FSKR). Although the two are merging, the combined entity will continue to be known as FSK.

Once the merger is complete, FSK will have over $14 billion in assets. The increased scale will give the new giant BDC access to capital markets on more favorable terms and create cost savings.

Management has indicated the new dividend yield will be 9.5% on the new BDC’s net asset value (NAV). Based on the projected NAV of $24.46 when the merger closes, that will be an annual payout of $2.32.

That’s a yield of over 13%…

There is also upside to NAV of over 30%.

Once the deal is done a $100 million buyback program will also be instituted.

You could buy either BDC here, but I’m partial to FSK Capital corp II (FSKR) as it has more firepower available for investment right now and a little less leverage. I doubt there will be any problems closing the merger but just in case there is, I would prefer to walk away owning FSK Capital corp II (FSKR).

The combined entity will be the second largest Business Development company in the United States.

Let’s Take a Look at the Largest BDC…

Ares Capital Corp. (ARCC) is affiliated with Ares Management, an alternative credit and private equity firm that has achieved enormous success in private markets. The BDC has also done very well for its investors with double digit returns over the last decade.

Since their IPO in 2004, Ares Capital Corp. has invested about $63 billion with a Gross Internal rate of return (IRR) of 14.3%. The total return of Ares Capital Corp. as of the end of 2020 was about 50% more than the S&P 500.

These guys are very good at making money in private credit and this BDC gives you a chance to share the wealth they create.

They are even better at not losing money as they have one of the lowest loan loss rates of any leveraged lender. First Lien Loan losses are .10 % of loans and second lien loans are just .20%. That’s about 10% of the industry averages for both classes of loans.

Ares is in outstanding financial shape with deep access to capital. They are one of the few BDCs to achieve an investment grade rating from all three major credit agencies.

Ares Capital Corp. trades right around NAV right now and has a yield of over 8%.

What to Pay For These Two BDCs

You can buy FS/KKR almost with abandon at current levels. I expect the market to look at the combined BDC’s very favorably and we will see the price slide up towards NAV. In the meantime you will be paid handsomely to own the shares

With ARCC it’s probably best to buy a little bit and then, as Henry McVey of KKR advises, look to lean into disruption in equity and credit markets to build a larger position.

Today we took a look at BDC’s from the private equity side of the building…

Next week, we will look at BDC’s with more of a venture capital spin to their investing strategy.