There’s no ignoring it.

Options trading, meme stocks, cryptocurrencies, SPACs, and new-paradigm tech plays are the capital markets’ new “Kool-Aid.”

And just about every investor is drinking it.

In doing so, however, those folks are missing out on a slice of the market that could bring them 3x or 4x gains – and at stunningly low levels of risk.

The sector: Bank stocks.

But not just any bank stocks. We’re talking about the small, off-the-radar regional and community banking firms that fit one or all of three intriguing storylines.

To zero in on this huge opportunity, we sat down with Takeover Targets editor, Tim Melvin, a veteran investor and market prognosticator who’s known as one of the industry’s foremost experts on banks and income investing.

In our wide-ranging interview, Tim tells us what’s in store for banks, interest rates, and the economy through the end of this year and into 2022.

He also spotlights the three storylines investors should play right now. And he recommends three banks any interested investors should take a look at.

For good measure, Tim also tossed in an income stock you can trade for boosted gains, and a fund that can act as a foundation for your financial-investing forays.

Here’s an edited transcript of our talk.

Let’s do a little bit of “scene-setting” here. With a big-picture view of banks. A decade after the Great Financial Crisis and “Great Recession” that very nearly brought down the global financial system, how does the banking sector look today? Is it healthy? Is it growing? If you had to give it a report-card letter grade, what would it be? And why?

Tim Melvin: There’s no equivocating here: You absolutely have to give the banking industry an “A+” for its performance in 2020 and 2021… especially the community banks.

Because of the regulatory changes that followed the Great Financial Crisis – and the consistency of the economic recovery we’ve had – banks traversed those two years in the best shape they’ve been in for at least the last century.

The best shape in the last 100 years? That’s impressive.

TM: That’s right. Capital levels were the highest they’ve ever been. And that meant that banks were extremely well-positioned and prepared for what came at them when the COVID-19 pandemic hit last year.

Loan portfolios were also in fantastic condition as well – since bankers had been much more conservative in their approach to lending in the post-GFC era. We had very limited loan losses on the books of the banking industry as we came into 2020.

These smaller banks also did an unbelievable job of processing PPP loans for businesses. Bankers were calling customers and helping them get the paperwork done so they could meet payroll and keep the lights on.

That last point is actually quite fascinating. It harkens back to the “old days” of customer service when your local clothing shop knew every customer and knew their preferences.

TM: That’s true, and it’s why I mentioned the anecdote about the PPP loans. In this era of data analytics and everything-over-the-web, personal customer service is still held in high regard. And it’s a competitive advantage that banks – particularly community banks – continue to have.

Let’s get a bit more specific and “categorize” the banking sector for readers. Give us your breakdown on the sector – with a “thumbnail” descriptor of each one … and its general health.

TM: The banking sector has a few different subsets.

The first one is the major money-center (MNC) banks. These are the big guys like JPMorgan Chase (NYSE: JPM), Goldman Sachs (NYSE: GS), Bank of America (NYSE: BAC) and Citigroup (NYSE: C). These are the banks that dominate the overall banking industry. Not much happens in the U.S. economy without the cash passing through these banks in some form or another. They are involved in just about anything involving money.

These banks tend to earn higher returns on equity (ROE) than smaller banks – thanks, in part, to the range of activities that they can be involved in … and the fact that they have the size/scale to apportion costs over an enormous pool of assets.

The economy is in decent shape thanks to the U.S. Federal Reserve and the relief programs passed last year. The markets have been strong and capital-market activity is robust. The large banks are hitting on all cylinders. They all passed the Fed’s stress test this year and are raising dividends and buying back enormous amounts of stock.

So it sounds good for the MNCs. What about their smaller brethren?

TM: The “larger regionals” is another subset that are also in pretty good shape right now.

These banks tend to focus more on basic banking services. And the COVID financial measures have helped them stand up to the challenges of the past year. Earnings have declined during the pandemic, but loan quality has held up well and capital levels remain very high.

Then there are the community banks … one of your real areas of specialization, right?

TM: Community banks have always fascinated me – it’s where I really cut my teeth as a banking analyst. And it’s where I consistently find opportunity, since small banks are widely misunderstood and consistently underfollowed by the big Wall Street brokerage houses.

Plus, community banks have been the superstars of the pandemic. They have done an incredible job of working with customers to deal with problems and have worked tirelessly to process PPP loans for their customers. There are countless stories of bankers reaching out to customers to help them process the paperwork and obtain the funds needed to keep their business alive.

Deposit growth has been high for community banks – in large part because of PPP loans. The pandemic has also given these banks a chance to compete with the larger banks. And let me tell you … many of them have taken full advantage of the opportunity.

Okay, now that we have covered the different sectors, what are some predictions you have about the banking sector?

TM: Talking about predictions, there are some very intriguing possibilities.

Let’s formalize this a bit here …

- Dealmaking Will Increase: This is probably the easiest prediction to make. M&A activity is going to continue to accelerate as we hopefully move closer to the end of the pandemic. We have seen some acceleration already. But given that the post-pandemic world will be even more difficult for smaller banks than at any point in the past decade, dealmaking will increase. I expect to see many more larger banks looking to acquire smaller, community banks over the next few years.

- The Digital Shift Will Separate the Winners From the Losers: This, too, is a pretty safe prediction to make – saying that the shift to digital banking will continue. The pandemic accelerated the acceptance of digital banking by as much as a decade. Even Grandpa and your grouchy old uncle can now accept the idea of doing their banking over the Internet. The reason this prediction is important is due to what it means: The banks that do the best job with digital and mobile offerings will have a huge advantage; those that struggle will be sticking “For Sale” signs in their front windows.

- Rates Will Rise – And Banks Will Win: I think we have finally seen the bottom in interest rates – and that they will finally begin to climb again. I also believe we will see banks benefit from those rising rates over the next several years. That should raise net interest margins for most banks, making them much more profitable.

Let’s put your banking-industry expertise to work here and conduct our own “SWOT Analysis” of the banking sector – looking at the strengths, weaknesses, opportunities and threats that are in play right now …

TM: Sounds great – let’s get started.

Let’s begin with “strengths.”

TM: The banking industry’s biggest strength right now is the very high level of capital it has. The industry is financially strong enough to meet any economic challenges. Loan quality is high enough that we should not see any problems with credit unless the COVID variants shut down the economy again.

Also, for the most part, banks have done a pretty great job of managing the technology shifts that we’ve seen in the past year. The adoption rate of online and mobile banking accelerated dramatically in 2020. And the bigger banks, in particular, did a fabulous job of keeping up with the changes.

In a sense, another one of the banking sector’s biggest advantages now is today’s economic environment.

Banks really ignored the stock-market recovery in 2020 until it was announced that vaccines would be available by year end. Once we knew that, bank stocks really took off – with the SPDR S&P Regional Banking ETF (NYSE: KRE) doubling in price since late October of last year.

Bank stocks have pulled back recently as the hoped-for higher interest rates never materialized. With inflation news still dominating the headlines, investors were hoping we’d see a steepening of the yield curve that would raise net-interest margins.

We have not seen that yet. But it’s still possible. Low, steady inflation that drives rates higher would be fantastic for bank-stock prices over the rest of 2021 and into 2022.

Ok, let’s move onto the “weaknesses” part of our SWOT analysis – using the same internal and external reference points as we did with strengths. What stands out here?

TM: The only weakness in the sector right now are those tight spreads. It is tough to make money when net-interest margins are flirting with all-time lows.

Size is also something of an issue for many banks. JPMorgan can afford to spend billions on technology and cybersecurity. But the smaller banks are going to have a hard time keeping up with the big guys.

The biggest weakness is one that seems to show up over and over again. And it’s one that banks create for themselves.

I’m talking about the propensity of bankers to “reach” for an additional 100 basis points in yield.

And by “reach,” you mean …

TM : Making moves where any extra yield to the bank is far outweighed by the risk incurred. And where that risk nearly always bites the industry right in the old assets.

I’ve seen this scenario play out over and over again – from era to era to era – with junk bonds, mortgage loans, loans to third-world nations and credit-default swap … and a host of other stupid choices that crush the whole sector.

Thankfully, it has yet to show up in this cycle.

“Opportunities” should be next up in our SWOT analysis. But let’s skip over that for a moment and instead delve instead to the “T” category –banking-sector threats.

TM: The biggest threat to the banking system comes from “nonbank” financial companies. Among the largest of these are the big tech companies like Alphabet/Google (Nasdaq: GOOGL), Amazon.com (Nasdaq: AMZN), Microsoft (Nasdaq: MSFT) and, of course, Apple (Nasdaq: AAPL).

To companies like these, financial services and payments are just an element of their business, an adjunct to their “ecosystem” and an additional service to offer their customers. But because these companies have such massive installed user bases (customer bases), anything these firms do that’s financial in nature are de facto threats to the banking industry.

And there are some recognizable “Fintech” names that are threats, too … right?

TM: Absolutely.

You’re talking about such nonbank-financial-payment fintechs like PayPal (Nasdaq: PYPL) and Square (NYSE: SQ). Those are the first two that come to mind, but there are dozens of these companies – with more popping up every day. Again, millennials and younger consumers are far more comfortable acting outside the FDIC-insured world than older folks. Granted, many of them have yet to experience a true down market or banking crisis – and their comfort level could shift when rough waters return.

Nonbank lenders will also continue to put pressure on the banking system. Many of these lenders are using fintech to underwrite and process loans and are getting the job done much faster than many community banks could ever hope to. The bigger banks are starting to use the same type of software to process loans. So they are much more competitive in this area than the smaller regional and community banks are positioned to be.

Cybercriminals are also an enormous threat and huge potential cost to the banking system.

Banks are dealing with millions of attacks each and every day. And that’s not going to end – ever. Customer breaches will be costly – both in dollar and reputational terms. In fact, given that the reputational hit can be disastrous, banks must understand that they have to spend the money to prevent this – no matter how much it might squeeze the bottom line.

What about cryptocurrencies? Are they a threat?

TM: You know, I just don’t view cryptocurrencies as being a big threat to the banking system at this time. We may eventually have a “FedCoin” that is part of the Federal payments system. But that will be part of the banking system – not a threat to it.

Among smaller banks we have seen a succession problem developing. There is no one to take over from the aging current management. The aspiring leaders in the talent pool are focused on – even obsessed with – Wall Street and Silicon Valley these days, so it’s getting tough to find qualified executives.

Banks are also dealing with a White House administration that’s decidedly less friendly than its predecessor. A lot of the regulations that the Trump Administration rolled back will now be reinstated. Here under a Biden presidency, there will be significant pressure for Congress and the regulatory agencies to increase the number of rules and to add more-restrictive policies.

That’s not great.

There is also a very realistic chance that corporate tax rates will be hiked – a change that will crimp community-bank profits in a big way.

That brings us to our favorite part of the SWOT analysis – the “opportunities.” Let’s get into some specific plays, now. Is there an ETF or fund that you view as a good “foundational” play for investors looking at banks or financial-services plays.

TM: Truth be told, I prefer individual stocks. I love the upside. I love the control it gives you.

That said, if your preferred approach is to own the whole sector, you need to own the First Trust NASDAQ ABA Community Bank Index Fund (Nasdaq: QABA) ETF. The real opportunity is in community banks and this ETF does a decent job of capturing the returns of this sector.

How about a bank-related income play?

TM: On the income side of the house I like owning Angel Oak Financial Strategies Income Term Trust (NYSE: FINS). This is a closed-end fund that invests in the debt securities issued by community banks. This debt can usually only be owned by institutions, so it represents a really unique opportunity for individual investors. The fund currently pays a dividend of 7%-plus, which is paid out monthly.

The shares are also trading at a small discount to net asset value.

Okay, you’ve given us two funds, but a moment ago you said you really prefer individual stocks. What are your favorites right now? And why?

TM: I like to divide my bank investing into three real strategies: Takeover Targets, Conversions, and Micro-banks. I’ll give you a pick for each.

Okay, let’s start with Takeover Targets.

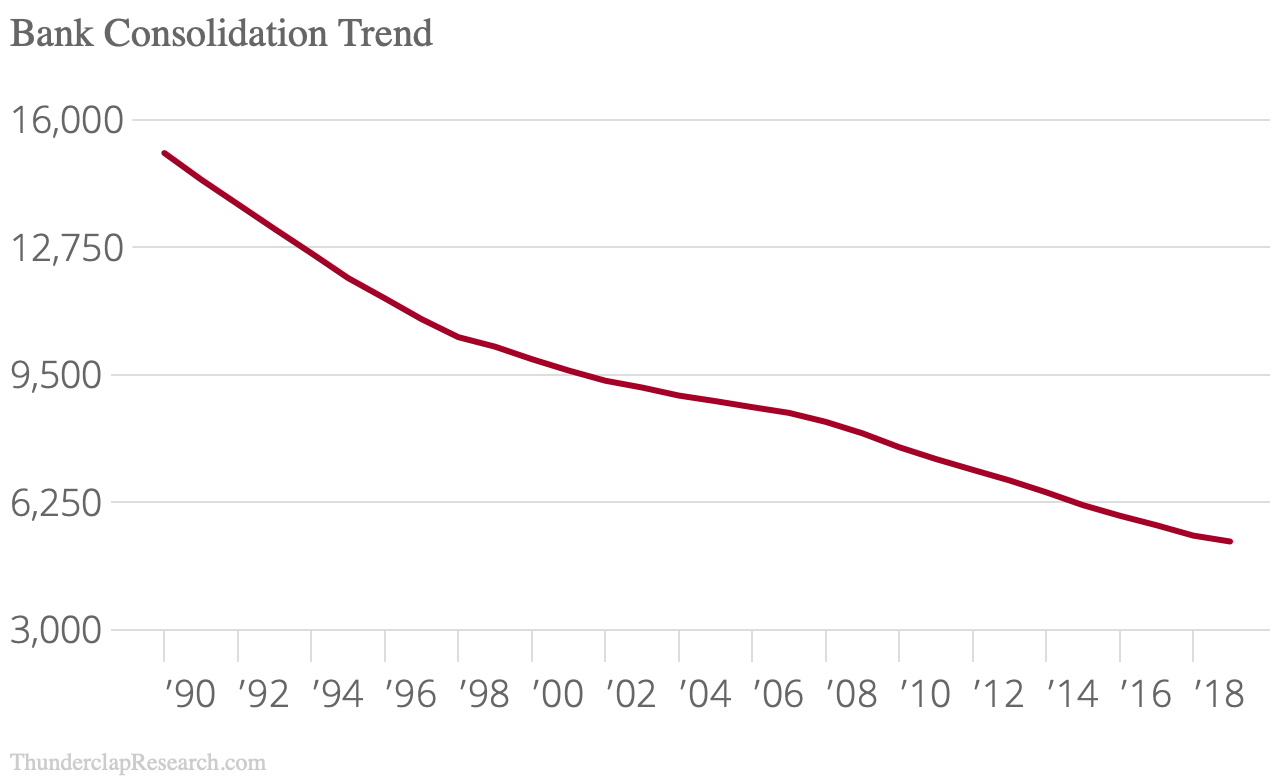

Takeover targets refers to the wave of dealmaking in banks that got its start way back in the middle-1980s when the Reagan Administration relaxed the interstate banking laws. Since then, we have watched the number of banks plunge from 18,000 then to around 6,000 today.

And this trend isn’t close to over. We still have way too many banks in the United States. Buying small banks trading at low multiples of tangible book value (BV) – and that have at least one activist investor pushing for a sale of the bank – will continue to be a wildly successful strategy.

Here we can focus on Peoples Financial Corp. (OTC: PFBX), an institution with $768 million in total assets and 18 branches along the Mississippi Gulf Coast. The bank is trading at about 80% of tangible book value right now. And at least one investor thinks change is needed…

Joseph Stilwell has been involved with banks for decades and has been involved in more than 70 activist campaigns in the last 20 years – with outstanding results. He currently owns 9.9% of the bank and has nominated a representative for the board of directors and is pushing hard for change at the bank.

The stock is at 80% of Book Value and a sale would bring a valuation of at least 125% of book, or roughly $24.65. The stock was recently trading at about $16.

Stilwell wins more than he loses. And he doesn’t give up easily.

Ok, let’s discuss the second theme – conversions.

TM: Thrift conversions are a true value-creation opportunity. Often we can buy these stocks at a substantial discount to tangible book value in the days and weeks after the offering.

Buying mutual thrifts is a long-term strategy. There is a three-year change-of-control prohibition and they can pay dividends or buy back stock for a year. These stocks will bore you until the day you get up and find that the bank has been taken over for three or four times what you paid for it.

Post-offering, the banks have an enormous amount of capital. Also, buybacks and dividends generally start at the one-year mark and grow from there. They will have excess capital from the IPO. And the loan portfolios are generally very conservative.

The thrifts tend to have a lot of U.S. Treasury and municipal bonds on the books, as well. When you look at that all together, you realize that a newly-converted thrift is one of the safest investments you can buy.

My favorite conversion pick right now is Northeast Community Bancorp Inc. (Nasdaq: NECB). The stock is trading at about 77% of book value at current prices – and has an enormous amount of excess capital from the offering.

Northeast is based in White Plains, N.Y. It has three full-service branches in New York; three full-service branches in Massachusetts; one full-service branch in Rockland County; two full-service branch offices in Orange County; and a loan-production office in New City, N.Y.

Northeast Community is a second-step conversion, so it’s permitted to pay dividends. And the dividend yield at the current price is a little over 2%.

So that leaves us with the last theme, Micro-banks.

TM: Buying regional and community banks that trade for less than 12 times earnings and pay a dividend of 3% or more is a wildly profitable approach to investing in bank stocks.

The benefit here is that, unlike most stocks people talk about these days, these companies are often deeply discounted as they are virtually uncovered by Wall Street analysts.

The strategy has crushed the overall market by close to a 2-to-1 margin over the last 10 years and by almost 4-to-1 over the past 20 years.

And right now, there’s one I really like…

It’s a Low-P/E, high-yield stock: Northwest Bancshares Inc. (Nasdaq: NWBI).

Northwest Bancshares is a medium-sized bank in Northwestern Pennsylvania, with 170 community-banking locations in Central and Western PA., Western New York and Eastern Ohio.

The bank has been around since 1896 – so it’s been through a business cycle or two.

At a recent price of about $13, Northwestern Bancorp shares were trading at just about 10 times earnings were yielding about 6%. The bank has paid dividends for 107 quarters in a row.

This has been a terrific conversation, Tim. It’s clear why you’re so respected as an expert on small-bank investments. Readers are going to love this. We’re appreciative – and we hope to do this again.

TM: Anytime.

Editor’s Note: Since 2013, Tim has recommended more than 100 banks without a single loss. Let me say that again… Over 100 recommended trades. ZERO losses.

Not only that, but 53 of his recommendations have been taken over or closed for an average gain of more than 81%.

And for a limited time, Tim is giving interested investors access to his ENTIRE portfolio. To learn more click here.